Что такое сейвинг аккаунт

Как зарабатывать на криптовалютах до 15% в год. Сейвинг и лендинг на криптобиржах

В условиях непрерывного развития рынка криптовалют и роста числа инвесторов, криптовалютные биржи, включая ZB, Binance предлагают трейдерам дополнительные сервисы для пассивного получения дохода.

С традиционными банками, предлагающими удручающе низкие процентные ставки по депозитам, сейчас подходящее время для изучения различных способов вложения свободных денежных средств.

Конечно, стейкинг на волатильные PoS-монеты может не оправдать ожиданий, как IEO или мастерноды в прошлом году.

Помимо стейкинга, мы также отслеживаем платформы, которые предлагают дополнительные формы пассивного получения дохода, например «crypto interest account» или «Savings».

В данной статье мы рассмотрим какие биржи предлагают самые выгодные проценты по сберегательным счетам в криптовалюте (услуга «Savings» или «Lending» на криптобиржах).

Что такое услуга сейвинг на криптобиржах?

Сейвинг простыми словами, это как сберегательный счет в банке, только в банке мы размещаем депозит в рублях или долларах и получаем с них %, а услуга Savings на криптобиржах предполагает, что мы размещаем на сберегательный счет криптовалюту и получаем % в криптовалюте.

«Ходлеры» могут получать привлекательную годовую доходность, просто паркуя биткойн на крипто-сберегательный счет. В конце данной статьи мы составим таблицу из ТОП-3 криптобирж, предлагающих самые высокие ставки по вкладам в криптовалюте.

Хотя это все еще спорно, тем не менее все больше людей начинают интересоваться преимуществами сберегательного счета в криптовалюте с начислением процентов, рассматривая «Crypto Savings» на криптобиржах как жизнеспособную альтернативу для получения пассивного дохода в криптовалютах BTC, ETH, USDT, XRP и др.

Лучшие сберегательные счета в криптовалюте предлагают до 14,6% процентов на стейблкоины и позволят вам заработать до 6% процентов на более популярных криптовалютах, таких как Биткоин и Эфириум.

Чтобы помочь вам найти лучший способ заработать пассивный доход на ваших криптоактивах, мы отделили пшеницу от плевел и выбрали наиболее конкурентоспособные предложения для запуска ваших цифровых активов в работу.

Если вы хотите заработать до 15% пассивного дохода на своих холодных крипто – или стейблкоин-сбережениях, то эта статья для вас.

Вот несколько savings-продуктов на которые мы обратили внимание:

При фиксированном депозите в BTC на срок 14 дней на Binance можно было заработать 3%, на срок 28 дней доходность составляла 3,25%. В настоящее время на Binance доступен только бессрочный тип депозита в BTC со ставкой 0.88%. При фиксированном депозите в USDT на 14 дней доходность составляет 7.77%, а при сроке депозита 30 дней 8.00%.

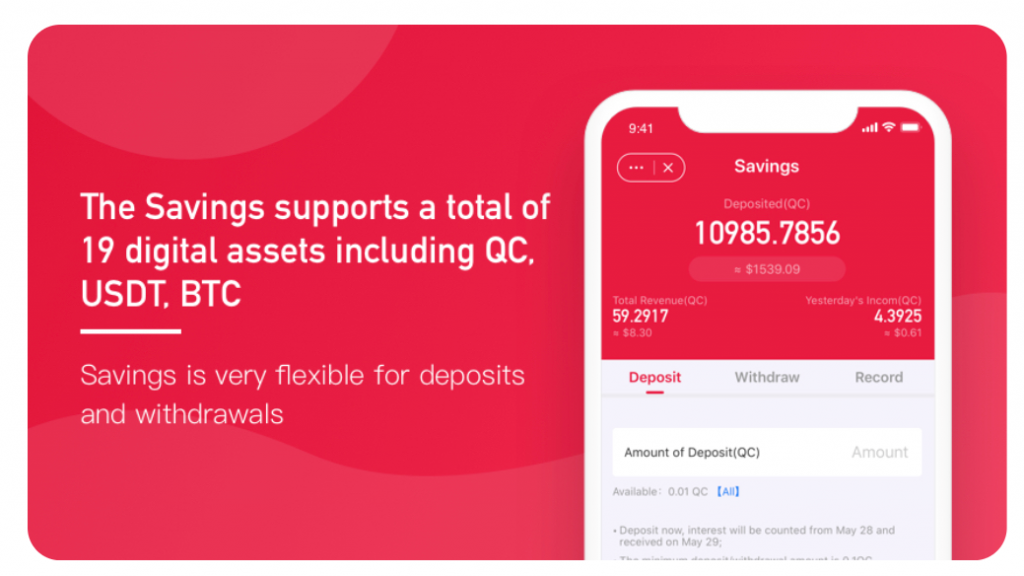

ZB.com Savings в настоящее время поддерживает 19 основных криптовалют, таких как BTC, ETH, EOS, XRP, BTS, QC и др. Годовая доходность при инвестировании с стейблкоин QC 14,6%.

Сейвинг (сбережения в криптовалюте под проценты) в стейблкоинах, вероятно, самый безопасный способ заработать деньги с помощью криптовалюты – так что мы рекомендуем вам присмотреться к этому тренду.

Не призрачный доход. Как заработать на стейблкоинах

Инвестиции в стейблкоины действительно могут быть интересны инвесторам, которые не любят рисковать.

Стейблкоины не подвержены высокой волатильности. К тому же стейблкоины обладают присущей им полезностью, особенно в периоды кризиса и рецессии.

Пользователи покупают все больше и больше стейблкоинов, чтобы хеджировать свои валютные риски, поэтому спрос на стейблкоины будет всегда.

Стейблкоин — это криптовалюта, обеспеченная определенным традиционным активом: фиатной валютой (долларом, евро, юанем), драгоценным металлом, природным ресурсом.

Владельцы некоторых стейблкоинов могут зарабатывать на среднесрочных и длительных инвестициях без рисков. К примеру, держатели QC могут получать до 14,6% прибыли ежегодно. Курс QC привязан к ценности китайского юаня в соотношении 1:1. На сегодняшний день QC является самым крупным и популярным азиатским стейблкоином.

В настоящее время, сейвинг стейблкоина QuickCash (QC) доступен только на бирже ZB.com. Сравнивая доходность QC с USDT, самым крупным стейблкоином в мире, доход по сберегательному счету в QC действительно самый высокий в отрасли, доход при депозите в USDT составляет всего 5,48-8%.

Почему инвесторам выгодно покупать стейблкоины

Стейблкоины — один из главных инструментов фиксирования прибыли. Совершив удачную сделку, трейдеры могут не выводить средства в фиат, а перевести активы в стейблкоины в ожидании лучшего периода на крипторынке.

Ниже мы проанализировали лучшие крипто-сберегательные счета для стейблкоинов, Bitcoin, Ethereum, альткоинов и выбрали лучшие платформы.

ТОП-4 криптобирж, предлагающие сэйвинг криптовалют

| Stablecoins | Bitcoin | Ethereum | |

| ZB.com | 14,60% | 2,85% | 2,58% |

| Binance | 8.30% | 0.88% | – |

| OKEX | 2,67% | 0,64% | 1,28% |

| Coinbase | 0,15% | – | – |

Вся информация в таблице взята из публичных официальных ресурсов

Давайте рассмотрим 4 лучших криптобиржи, которые предлагают услуги сейвинга (вклады в криптовалюте под проценты) для заработка пассивного дохода на криптовалютах.

ZB.com Savings: Лучшая годовая доходность в Crypto Savings

ZB.com – это ведущая в мире криптовалютная биржа, которая появилась в 2013 году и на сегодняшний день является одной из самых крупных площадок по объему торгов и предоставлению услуг в сфере крипто трейдинга.

На ZB имеется большое количество инструментов для трейдинга и заработка, включая маржинальную торговлю, стейкинг, сейвинг и крипто-кредиты для заемщиков.

ZB Savings — это возможность осуществлять депозиты под проценты в виде BTC, USDT, ETH, XRP и других криптовалютах.

На сегодняшний день, на ZB.com доступен savings в 19 валютах. Инвесторы могут открыть сберегательный счет в криптовалюте на ZB и зарабатывать до 15% на своих цифровых активах.

| Криптовалюты | Годовая процентная ставка на ZB.com |

| QC | 14,60% |

| BTC | 2,85% |

| USDT | 2,59% |

| ETH | 2,58% |

| XRP | 1,93% |

| EOS | 2,70% |

| XLM | 2,35% |

| LTC | 2,95% |

| ADA | 8,43% |

| DASH | 5,50% |

ZB interest rates, данные 8 июня 2020

Преимущества ZB Savings

- ZB предлагает самые высокие проценты на крипто сбережения

- Поддерживает более 19 криптовалют для сейвинга

- ZB.com Savings доступен в мобильном приложении как на Android, так и на IOS (мобильное приложение биржи доступно на русском языке).

- Поддержка криптовалютного процентного счета в стейблкоине QC со ставкой 14.6%.

- Отсутствуют требования по минимальному лимиту для суммы сбережений.

Доход будет рассчитываться со второго дня, вознаграждение поступит на счет на третий день.

Пользователи могут вносить и выводить средства в любое время.

2. Binance Savings: бессрочные и фиксированные депозиты

Лендинг на Binance предлагает два варианта крипто депозитов:

- бессрочные депозиты и

- фиксированные депозиты.

Фиксированный депозит означает, что вы блокируете свои внесенные средства на определенный срок и более высокие проценты.

Бессрочные депозиты, с другой стороны, позволяют вам выводить свои средства в любое время, а процентная ставка может меняться со временем.

| Криптовалюты | Годовая процентная ставка на Бинанс |

| BTC | 1% |

| EOS | 3.80% |

| COCOS | 4% |

| USDT | 7.53% |

| BUSD | 7.88% |

| ONE | 8% |

Данные по фиксированным сбережениям на Binance, 8 июня 2020

Преимущества Binance Landing

- Binance – ведущая в мире криптовалютная биржа

- Поддерживает дебетовые и кредитные карты

- Поддерживает два варианта крипто депозитов – бессрочные депозиты и фиксированные депозиты

- Удобный интерфейс

3. OKEX Savings

OKEX предлагает два варианта крипто лендинга – бессрочные депозиты и фиксированные депозиты на 30, 60 и 90 дней.

Начисленные крипто проценты выплачиваются в той же валюте, что и ваш депозит.

| Криптовалюты | Годовая процентная ставка |

| BTC | 0.64% |

| ETH | 1.28% |

| DASH | 1.29% |

| XRP | 1,64% |

| BSV | 1.16% |

| BCH | 0.84% |

| USDT | 3.36% |

OKEX interest rates при бессрочном депозите, 8 июня 2020

- Поддерживает более 20 криптовалют, включая BTC, ETH, BCH.

- Инвесторы могут зарабатывать до 4.82% при размещении крито-депозита в EOS на 90 дней.

4. Coinbase – депозиты в стейблкоине USDC

Держатели USD Coin на бирже Coinbase ранее могли получать доход в размере 1,25% годовых. Но в июне 2020 Coinbase снизили ставку до 0.15%.

На момент публикации, USDC является 22-й по величине криптовалютой, имеющей капитализацию около $735 млн.

Что такое crypto interest account?

Депозит в криптовалюте под процент работает во многом так же, как и сберегательный счет, который вы имеете в своем местном банке.

Однако вместо того, чтобы вносить наличные деньги, чтобы заработать проценты на свои доллары или евро, вы вносите криптовалюты и получаете проценты взамен.

Когда несколько лет назад был введен первый депозит в криптовалюте Bitcoin (BTC) с начислением процентов, он был встречен со здоровой долей скептицизма.

Это было связано с тем, что первоначальные спонсоры были небольшими стартапами без надежной финансовой основы или поддержки.

Перенесемся в настоящее время, сберегательный счет в криптовалюте (savings, lending) и стейкинг (Staking) стали популярным выбором среди сообщества для заработка пассивного дохода на криптовалютах, и несколько крупных авторитетных криптобирж (ZB.com, Coinbase, Binance, OKEX) предоставляют эти услуги.

Зачем биржам лендинг криптовалют?

Криптобиржи зарабатывают деньги, одалживая ваши монеты заемщикам по более высокой ставке, чем они платят вам в качестве процентов – точно так же, как работают банки.

Процентные ставки по традиционным сберегательным продуктам обычно низкие, и поэтому криптовалютные активы кажутся очень привлекательными, причем некоторые платформы, такие как ZB.com, Binance предлагают процентную ставку до 15% на стейблкоины и до 18% на более волатильные, экзотические токены малой капитализации и альткоины.

Самые важные вещи, на которые следует обратить внимание прежде чем решить, куда положить свои деньги – это процентная ставка, частота ее начисления, комиссия за вывод средств, безопасность платформы и кошелька, в котором хранятся ваши средства.

Вы всегда должны искать платформу, которая предлагает регулируемое, застрахованное, холодное хранение, чтобы обеспечить максимальную безопасность ваших криптоактивов.

Рассмотренные выше криптобиржи соответствуют необходимым требованиям.

Преимущества крипто депозита под проценты (crypto savings account)?

- Вы держите деньги в криптовалюте, поэтому помимо %, который вам будут начислять, у вас есть возможность заработать и на самом курсе криптовалюты.

- Что касается крипто-депозита под проценты в стейблкоинах, то это, вероятно, самый безопасный способ заработать деньги с помощью криптовалют.

- В любой день вы можете вывести свои деньги с прибылью, которую получили.

Есть ли фиксированный срок при крипто депозите под проценты?

Каждая криптобиржа предлагает различные условия в отношении сроков крипто-депозита. Некоторые предлагают гибкие условия, которые означают, что вы можете вывести свои средства в любое время. Некоторые предлагают варианты депозитов на 1 месяц, 2 месяца или 3 месяца.

Есть важный момент! Когда выбираете какой криптоактив отправить на Сбережение (Savings) обязательно проверьте, есть ли она у вас в стейкинге, так как именно второй обычно выгоднее.

Посетите нашу страницу с обзором как зарабатывать на стейкинге криптовалюты, чтобы найти монеты и лучшие криптовалютные биржи, предлагающих самые высокие вознаграждения за стейкинг монет.

Как заработать на Криптобирже БЕЗ ТРЕЙДИНГА. Часть 2: Лендинг Криптовалют [Savings]

В предыдущей статье мы рассмотрели стейкинг криптовалют на криптобиржах, как способ получения пассивного дохода.

В данной статье мы рассмотрим получение пассивного дохода на сейвинге (лендинге) криптовалют. Сейвинг на криптобиржах или так называемые криптовалютные процентные счета (crypto interest account) набирают популярность. Все больше людей начинают интересоваться преимуществами сберегательного счета в криптовалюте с начислением процентов, рассматривая crypto savings на криптобиржах как жизнеспособную альтернативу для получения пассивного дохода c криптовалют BTC, ETH, USDT, XRP и др. Лучшие сберегательные счета в криптовалюте предлагают до 14,6% в стейблкоинах и до 6% при инвестировании в основные криптовалюты, такие как Биткоин и Эфириум. При этом вывести криптовалюту можно в любой момент.

Что такое Crypto Savings Account или Savings на криптобиржах ?

Криптовалютные процентные счета можно сравнить со сберегательным счетом в банке, только в банке мы размещаем депозит в рублях или долларах и получаем с них %, а услуга Savings на криптобиржах предполагает, что мы размещаем под проценты криптовалюту.

Преимущества криптовалютного процентного счета (crypto savings account)?

- «Ходлеры» могут зарабатывать привлекательную годовую доходность просто паркуя биткойн на крипто-сберегательный счет;

- Помимо % который вам будут начислять по крипто-депозиту, у вас есть возможность заработать и на росте курса криптовалюты;

- Сейвинг в стейблкоинах (криптовалютные процентные счета в USDT, USDC, QC и др.), вероятно, самый безопасный способ заработать деньги с помощью крипто, т.к. cтейблкоины не подвержены высокой волатильности;

- Вывести средства можно в любой момент с прибылью, которую вы получили.

Примечание: Заработок на хранении монет не гарантирует баснословной прибыли, но это хорошая возможность криптовалютного заработка на свободных средствах, которые хранятся на крипто-депозите как инвестиции. При правильном подходе можно получить хороший пассивный доход.

Инвестиции в стейблкоины

Владельцы некоторых стейблкоинов могут зарабатывать на среднесрочных и длительных инвестициях без рисков. К примеру, доход при крипто-депозите в USDT составляет 5,48-8%, а держатели стейблкоина QC могут получать до 14,6%. Курс QC привязан к ценности китайского юаня в соотношении 1:1. На сегодняшний день QC является самым крупным и популярным азиатским стейблкоином.

Инвестиции в стейблкоины действительно могут быть интересны инвесторам, которые не любят рисковать. Стейблкоины не подвержены высокой волатильности. К тому же стейблкоины обладают присущей им полезностью, особенно в периоды кризиса и рецессии. Пользователи покупают все больше и больше стейблкоинов, чтобы хеджировать свои валютные риски. И наконец, стейблкоины — один из главных инструментов фиксирования прибыли. Совершив удачную сделку, трейдеры могут не выводить средства в фиат, а перевести активы в стейблкоины в ожидании лучшего периода на крипторынке.

Сейвинг и Лендинг на криптобиржах

Самые важные моменты, на которые следует обратить внимание прежде чем решить, куда положить свои деньги — это процентная ставка, частота ее начисления, комиссия за вывод средств, безопасность платформы и кошелька, в котором хранятся ваши средства. Вы всегда должны искать платформу, которая предлагает регулируемое, застрахованное, холодное хранение, чтобы обеспечить максимальную безопасность ваших криптоактивов.

Мы составили таблицу и сравнили годовую доходность по криптовалютным процентным счетам в стейблкоинах, Bitcoin и Ethereum на четырёх крупнейших биржах — Coinbase, ZB.com, Binance и OKEX.

ТОП-4 основных криптобирж, предлагающие сейвинг/лендинг криптовалют

Найдите лучшие условия по процентным сберегательным счетам в криптовалюте

Информация из публичных официальных ресурсов. Годовая процентная ставка может меняться со временем. Всегда проверяйте исходные данные непосредственно на сайте соответствующей платформы.

Информация из публичных официальных ресурсов. Годовая процентная ставка может меняться со временем. Всегда проверяйте исходные данные непосредственно на сайте соответствующей платформы.

По состоянию на июнь 2020 криптобиржа ZB.com предлагает лучшую доходность по крипто-депозитам в BTC, ETH, а также в стейблкоинах.

ZB.com — это ведущая в мире криптовалютная биржа, которая работает на рынке с 2013 года и на сегодняшний день является одной из самых крупных торговых платформ по объему торгов и предоставлению услуг в сфере крипто трейдинга. На ZB имеется большое количество инструментов для трейдинга и заработка, включая маржинальную торговлю, стейкинг, сейвинг и крипто-кредиты для заемщиков.

Сервис ZB Savings предоставляет возможность осуществлять депозиты под проценты в виде BTC, USDT, QC, ETH и других криптовалютах. На сегодняшний день, на ZB.com доступны криптовалютные процентные счета в 19 валютах, пользователи ZB могут зарабатывать до 15% пассивного дохода на своих цифровых активах просто размещая их на своем криптовалютном процентном счете.

Сейвинг на ZB.com доступен на сайте и в мобильном приложении в разделе ZAPP. Скачать мобильное приложение ZB для Android и iOS: https://www.zb.com/download

Сейвинг на ZB.com доступен на сайте и в мобильном приложении в разделе ZAPP. Скачать мобильное приложение ZB для Android и iOS: https://www.zb.com/download

Преимущества ZB Savings

- Уcлoвия ZB.com Savings являютcя caмыми пpивлeкaтeльными в oтpacли;

- Биржа поддерживает более 19 криптовалюты для сейвинга;

- ZB.com Savings доступен в мобильном приложение как на Android , так и на IOS (мобильное приложение биржи доступно на русском языке);

- Держатели стейблкоина QC на ZB.com могут получать до 14,6%. Курс QC привязан к ценности китайского юаня в соотношении 1:1. На сегодняшний день cтейблкоин QCash (QC) является самым крупным и популярным азиатским стейблкоином;

- Отсутствуют требования по минимальному лимиту для суммы сбережений. Доход будет рассчитываться со второго дня, вознаграждение поступит на счет на третий день. Пользователи могут вносить и выводить средства в любое время.

Как зарабатывать на сейвинге криптовалют

Вам необходимо выбрать раздел Savings на криптобирже и выбрать монету, которую хотите отправить на крипто-депозит. Доход на каждой монете свой, поэтому смотрите то, что предлагает платформа.

Принцип работы сейвинга часто сравнивают с банковским депозитом, когда пользователь кладет деньги на счет под проценты на определенный период времени, и чем больше средств лежит на счету, тем больше прибыль. То же правило действует и для сейвинга криптовалюты.

Надеемся, что наши статьи помогут вам понять, как вы можете зарабатывать на цифровых активах.

Небольшое напоминание: Можно зарабатывать пассивный доход на стейкинге криптовалют, которые работают на алгоритме PoS.

Ознакомьтесь с нашей статьей о стейкинге, чтобы найти монеты и торговые платформы, предлагающих самые высокие вознаграждения за стейкинг.

Если вы еще не присоединились к нашему сообществу, мы доступны и активны на следующих социальных сетях:

Checking Account vs. Savings Account

A checking account is a type of bank deposit account that is designed for everyday money transactions. The money in a savings account, however, is not intended for daily use, but is instead meant to stay in the account — be saved in the account — so that it might earn interest over time. Savings accounts have higher interest rates than checking accounts, meaning it is better to let large sums of money (e.g., an emergency fund) sit in savings instead of checking. The fees and other criteria for checking and savings accounts — such as monthly account maintenance fees, minimum account balances, and interest rates — vary slightly from one bank to another.

Comparison chart

| Checking Account | Savings Account |

|---|---|---|

| Withdrawal Restrictions | None | Typically 3-6 withdrawals a month. Allowed to withdraw only a portion of the account balance. |

| Minimum Balance | Sometimes, varies by bank | Sometimes; varies by bank |

| Designed For | Regular use | Saving money risk-free for short- or long-term |

| Fees | Sometimes, varies by bank | Sometimes, varies by bank |

| Interest Earned | Nominal/none | Yes, but amount varies wildly by bank or credit union |

| Overview | A type of bank account that is designed for everyday money transactions. | An account that accrues more interest than a checking account does; intended for saving money. |

| Access | Any time | To use money, account holder must first transfer it to checking account (usually) |

| Other Features | Overdraft, external online transactions (money transfer, manual/automatic bill pay) | No facilities other than internal online transactions with some banks (i.e., transfer from savings to checking) |

Account Fees

Many banks require checking account holders meet some criteria; for example, to set up the direct deposit of paychecks into a checking account, the account owner must usually maintain a minimum balance or make a minimum number of transactions each month. When these criteria are not met, banks often charge users monthly maintenance fees. Banks may also impose ATM usage fees, overdraft charges, overdraft protection fees to avoid overdraft charges, and fees for online access and bill paying. These vary depending on the bank, with some banks and credit unions, like Ally, charging very few fees.

Most savings accounts are fee-free, as long as owners do not exceed their withdrawal limits. However, some banks, like Bank of America, require account owners keep a minimum daily balance or make a certain number of money transfers into the savings account every month to avoid account maintenance fees.

This short video explains the differences between savings and checking accounts:

Interest Rates

Checking accounts typically earn little to no interest, depending on the bank. Savings accounts always accrue interest. The interest rate depends on the bank, the type of savings account (e.g., see Money Market vs Savings Account), and the amount deposited, but is always higher than the interest rate on checking accounts.

As of May 2016, the highest interest rate on savings accounts (in the United States) is about 1%. [1] Online banks, like Ally and EverBank — those without traditional brick and mortar businesses — often offer higher-yielding accounts than can traditional banks, but some credit unions can be equally good, if not better.

Bill Pay

Several other online transactions are possible with a checking account. For instance, with online banking, an account owner can set up automatic bill pay for recurring payments like rent, water/electric bills, etc., and even make one-time payments.

Such transactions are usually impossible with a savings account, although one can transfer money from his or her savings account to a checking account.

Debit Cards

Checking accounts often come with debit cards that allow withdrawals from an ATM and pay for items in stores. Debit cards only allow users to spend money that is available in the account.

Savings accounts typically do not come with debit cards, so withdrawals must either be transferred to a connected checking account online, requested over the phone, or done in person at the bank.

Restrictions

There are no limits on the number of transactions (withdrawals and deposits) that can be made to or from a checking account.

Savings accounts are designed for occasional use, so they usually have restrictions on how often money can be withdrawn. The limit is typically three to six withdrawals a month, including electronic transfers and automatic payments. There is no limit to the number of deposits one can make into a savings account.

Usage

A checking account is typically used for regular spending and purchases, like paying bills, shopping for groceries, etc. While it is possible to withdraw money from a savings account at an ATM, by default ATMs withdraw cash from a checking account.

A savings account, as the name suggests, is used to save money for a longer period of time. The idea is to let that money accrue and not use it unless there is an emergency or until it is time to pay for college tuition or purchase a significant item, like a house or car.

References

- Wikipedia: Savings account

- Wikipedia: Transactional account

Related Comparisons

Money Market Account vs Savings Account

Money Market Account vs Savings Account CD vs Savings Account

CD vs Savings Account Loan vs Mortgage

Loan vs Mortgage Bank vs Credit Union

Bank vs Credit Union Debt vs Equity

Debt vs Equity Credit Security Freeze vs Fraud Alert

Credit Security Freeze vs Fraud Alert

- Follow

- Share

- Cite

- Authors

Share this comparison:

If you read this far, you should follow us:

“Checking Account vs Savings Account.” Diffen.com. Diffen LLC, n.d. Web. 2 Oct 2021.

Comments: Checking Account vs Savings Account

- Money Market Account vs Savings Account

- CD vs Savings Account

- Loan vs Mortgage

- Bank vs Credit Union

- Debt vs Equity

- Credit Security Freeze vs Fraud Alert

- E*TRADE vs Scottrade

- APR vs Interest Rate

Edit or create new comparisons in your area of expertise.

Difference B/w Current Account and Savings Account

Current Account vs Savings Account

- Savings accounts are suitable to build emergency funds, whereas current accounts facilitate regular business transactions.

- Unlike a saving account, current accounts do not have any limit on monthly transactions.

- You need to maintain a relatively higher minimum balance in a current account than a savings account.

- A saving account is suitable for individuals, whereas a current account caters to business organisations.

- Savings Account offers interest rates ranging between 0.50% to 7.25% whereas a current account does not provide any interest.

Sorry! You have exceeded your daily OTP limit. Please retry after 24 hours.

- MyLoanCare does not charge any fees for processing your application. Never pay any cash to anyone for your application.

- Never share your OTP with anyone.

Please Re-confirm Your Number

Please Re-confirm Your

- Savings Account Info

- Savings Account

- Savings Account Interest Rates

- Savings Account Documents

- How to Open Savings Account Online

- Types of Savings Account

- Savings Account Services

- Balance Check Enquiry

- Mobile Banking

- Online Internet Banking

- IMPS Fund Transfer

- RTGS Fund Transfer

- NEFT Fund Transfer

- UPI Facility

- Content on Page

- Savings Account

- Current Account

- Difference

- FAQs

Apply Now

Savings Bank Accounts v/s Current Accounts

Savings Account and Current Account are amongst the two most common and widely opened accounts in a bank. Savings Bank Accounts as the name suggests is for personal savings for a long term and allows account holders to save and earn interest on the savings. On the other hand, a current account is also known as a business account and is opened to ease off regular business transactions. Both the accounts can be opened at leading public and private sector banks such as State Bank of India, ICICI, HDFC Bank, Citibank etc. depending on your banking needs.

Savings Account

A savings account opened at a bank is a basic type of account that allows you to deposit money and keep it safe while earning moderate interest on the balance maintained in the accounts. Key features of Savings Account are mentioned below.

- A Savings Account provides fixed returns on your deposit. The rate of interest on a Savings Account varies from bank to bank, and it ranges between 0.50% to 7.25%.

- With a Savings Account, you need to maintain a low minimum balance in your account to keep your account activated. Some banks also offer Zero Balance Savings Accounts.

- Account-holders can withdraw funds from a Savings Account using ATM/ debit card.

- Savings Accounts are mostly suitable to save funds for emergencies. However, it does not provide an overdraft facility to the account holders.

Current Account

Current Account is a type of account that is opened by the people in business who have high regular transactions with the bank. Account holders can open the current account to ease off daily business transactions and get the following benefits with their current account.

- These accounts offer limitless cash withdrawal facilities and thus do not provide any interest.

- As a current account has no limits on deposits and withdrawal, therefore it involves high fees for facilitating corporate transactions.

- Account holders can also get overdraft facility with the Current Accounts.

- You can make payment via cheque, demand drafts, pay orders etc. for making payments against Current Accounts.

What is the Difference Between Current Account Vs Savings Account?

| Point of difference | Current Account | Savings Accounts |

|---|---|---|

| Purpose | It facilitates frequent business/financial transactions. | A saving account encourages and promotes savings by providing interest on money deposited on savings. |

| Ideal for | Current Account is suitable for businessmen, firms, companies, organizations, public enterprises, etc. who want to make regular business transactions. | Savings Account is meant for individuals and self-employed who want to save some money for small/big purchases, travel etc. |

| Minimum Balance | You need to maintain a relatively higher balance in a current account. The limit for the requirement of a minimum balance in a current account varies from bank to bank. | The requirement for minimum balance in a Savings Account is low. With some Banks, you may be required to maintain any balance in your account. |

| Monthly Transaction | There are no limits on the number of monthly transactions in a current account. | The number of monthly transactions in a savings account ranges from 3 to 5 transactions per month (financial and non-financial). |

| Interest | They offer zero or nil Interest. | The rate of interest on Savings Account ranges between 0.50% to 7.25%. |

✅ What is the difference between the savings account and current account in India?

A savings account is opened by individuals to save funds for personal needs or emergencies. Account holders can also earn interest on the savings account. On the other hand, a current account is mostly opened by people in business to conduct regular business transactions and does not offer any interest.

✅ How can I convert my savings account to my current account?

It is not possible to convert your savings account to a current account as both the accounts are different in nature and also have distinct features and benefits. While a saving account is meant for personal use and thus can be opened with basic documents for KYC. On the other hand, a current account requires you to submit documents for business existence as well.

✅ What is the minimum balance in my current account & Savings Account?

The minimum balance required in current and savings accounts varies from bank to bank. While some banks provide zero balance savings accounts, the requirement for maintaining a minimum balance in a current account is relatively higher in a current account.

Savings Accounts

- Overview

- How Interest Rates Work

- Annual Equivalent Rate (AER)

- Best Banks for Savings Accounts

- Overview

- Individual Development Accounts

- Linked Savings Account

- Christmas Club

- Overview

- How Savings Accounts Are Taxed

- Tax-Free Savings Accounts

- Places to Save Tax Free

- ABLE Accounts

:max_bytes(150000):strip_icc()/Julia_Kagan_1500x1616-color-web-9e40a05155ff4d31a9f4878dc6dd2431.jpg)

:max_bytes(150000):strip_icc()/IMG_7291_Crop-SomerAnderson-fdd793749683441487bbf0bd73328c59.jpg)

What Is a Savings Account?

A savings account is an interest-bearing deposit account held at a bank or other financial institution. Though these accounts typically pay a modest interest rate, their safety and reliability make them a great option for parking cash you want available for short-term needs.

If you’re ready to shop for a new savings account, we maintain a list of the best savings account rates we can find.

Savings accounts have some limitations on how often you can withdraw funds, but generally offer exceptional flexibility that’s ideal for building an emergency fund, saving for a short-term goal like buying a car or going on vacation, or simply sweeping surplus cash you don’t need in your checking account so it can earn more interest elsewhere.

Key Takeaways

- Because savings accounts pay interest but keep your funds easy to access, they’re a good option for parking cash you’ll want in the short-term or to cover an emergency.

- In exchange for the ease and liquidity that savings accounts offer, you’ll earn a lower rate than more restrictive savings instruments and investments might pay.

- The amount you can withdraw from a savings account is generally unlimited.

- The interest you earn on a savings account is considered taxable income.

How Savings Accounts Work

Savings and other deposit accounts are important sources of funds that financial institutions can turn around and lend to others. For that reason, you can find savings accounts at virtually every bank or credit union, whether they are traditional brick and mortar institutions or operate exclusively online. In addition, you can find savings accounts at some investment and brokerage firms.

The rate you’ll earn on a savings account is generally variable. With the exception of promotions promising a fixed rate until a certain date, banks and credit unions can generally raise or lower their savings account rate at any time. Typically, the more competitive the rate, the more likely it is to fluctuate over time.

Changes in the federal funds rate can also trigger institutions to adjust their deposit rates. And some institutions offer special high-yield savings accounts, which are also worth investigating.

Savings Account

Some savings accounts will require a minimum balance in order to avoid monthly fees or earn the highest published rate, while others will have no minimum balance requirement. So it’s important to know the rules of your particular account to ensure you avoid diluting your earnings with fees.

Whenever you want to move money in or out of your savings account, you can do so at a branch or an ATM, by electronic transfer to or from another account using the bank’s app or website, or by direct deposit. Transfers can usually be arranged by phone, as well.

Note, however, that while there are no dollar limits on how much you can withdraw from your account (in fact, you can empty it or close it at any time), federal law had capped the frequency of withdrawals from all U.S. savings accounts to six per monthly statement cycle until April 2020. Exceed the limit and the bank could charge you a fee, close your account, or convert it to a checking account. In 2020 the Federal Reserve suspended this limit. It is not clear if this change is permanent.

Just as with the interest earned on a money market, certificate of deposit, or checking account, the interest earned on savings accounts is taxable income. The financial institution where you hold your account will send a 1099-INT form at tax time whenever you earn more than $10 in interest income. The tax you’ll pay will depend on your marginal tax rate.

Savings Account Advantages

Savings accounts offer you a place to put your money that is separate from your everyday banking needs, allowing you to stash money for a rainy day or earmark funds to achieve a big savings goal. What’s more, the bank’s security measures, along with federal protection against bank failures provided by the Federal Deposit Insurance Corporation (FDIC), will keep your money safer than it would be under your mattress or in your sock drawer.

Beyond keeping your funds safe, savings accounts also earn interest, so it pays to keep any unneeded funds in a savings account instead of accumulating cash in your checking account, where it will likely earn little or nothing. At the same time, your access to funds in a savings account will remain extremely liquid, unlike certificates of deposit, which impose a hefty penalty if you withdraw your funds too soon.

Holding a savings account at the same institution as your primary checking account can offer several convenience and efficiency benefits. Since transfers between accounts at the same institution are usually instantaneous, deposits or withdrawals to your savings account from your checking account will take effect right away. This makes it easy to transfer excess cash from your checking account and have it immediately earn interest—or transfer money the other way if you need to cover a large checking transaction.

Many institutions allow you to open more than one savings account, which can be handy if you want to keep track of your savings progress on multiple goals. For instance, you could have one savings account to save for a big trip while a separate one holds surplus cash from your checking account.

Savings Account Disadvantages

The trade-off for a savings account’s easy access and reliable safety is that it won’t pay as much as other savings instruments. For instance, you can earn a higher return with certificates of deposit or Treasury bills, or by investing in stocks and bonds if your time horizon is long enough. As a result, savings accounts present an opportunity cost if used for long-term savings.

Also, while the liquidity of a savings account is one of its key benefits, it can also be a downside, as the ready availability of funds may tempt you to spend what you’ve saved. In contrast, it is much more difficult to cash in a bond, withdraw funds from a retirement account, or sell a stock than it is to take money out of your savings account, especially if that account is linked to your checking account.

Savings accounts are also a poor choice for funds you need to access frequently. Because rules previously restricted withdrawal transactions to six times per month—whether those were transfers or outright withdrawals at a branch or ATM—a savings account was not always an appropriate vehicle for these funds. The lifting of these restrictions has made the funds more accessible.

Fast and easy to set up, and to move money to and from

Can be conveniently linked to your primary checking account

Up to your full balance can be withdrawn at any time.

Up to $250,000 is federally insured against bank failure.

Pays less interest than you can earn with certificates of deposit, Treasury bills, or investments

Easy access can make withdrawals tempting.

Some savings accounts require minimum balances.

How to Maximize Earnings From a Savings Account

Although most major banks offer low interest rates on their savings accounts, many banks and credit unions provide much higher returns. In particular, online banks offer some of the highest savings account rates. Because they don’t have physical branches—or have very few—they spend less on overhead and can often offer higher, more competitive deposit rates as a result.

The key is to shop around, starting with the bank where you hold your checking account. Even if that institution doesn’t offer a competitive savings account rate, it will give you a frame of reference for how much more you can earn by moving your savings elsewhere.

As you shop for the best rates, however, beware of account features that can curtail your earnings, or even drain them. Some promotional savings accounts will only offer the attractive rate they’re advertising for a short period of time. Others will cap the balance that can earn the promotional rate, with dollar amounts above that maximum earning a paltry rate. Even worse is a savings account with fees that cut into the interest you earn each month.

How to Open a Savings Account

To set up a savings account, visit one of the bank or credit union’s branches, or establish the account online, for those institutions that offer it. You’ll need to provide your name, address, and telephone number, as well as photo identification. Also, because the account earns taxable interest, you’ll be required to provide your Social Security Number (SSN).

Some institutions will require you to make an initial minimum deposit at the time you open the account. Others will allow you to open the account first and fund it later. In either case, you can make your initial deposit with a transfer from an account at that institution, an external transfer, a mailed in or mobile deposit check, or a deposit in person at a branch.

How Much to Keep in Your Savings Account

The amount you keep in your savings account will depend on your goals for the funds, or your use of the account. If you’ve set up the savings account to sweep excess funds from your checking account, your balance is likely to vary regularly. In contrast, if you are building up to a savings goal, your balance will likely start low and increase steadily over time.

If you’ve instead established your savings account as an emergency fund, financial advisors typically recommend holding enough savings to cover at least three to six months’ living expenses, giving you a financial cushion in case you lose your job, face a medical issue, or encounter another money-draining emergency. However, some analysts recommend keeping only some of that emergency fund in a simple savings account, while moving the rest of it to an account or instrument that earns a higher return.

In any case, note that deposits at banks are covered by FDIC insurance and at credit unions, by NCUA insurance. Both of these protect each individual account holder at the institution for up to $250,000 in deposit balances, should the institution fail. For most consumers, this more than covers what they have on deposit. But if you are holding more than $250,000 in deposit accounts, you’ll want to split your balance across more than one account holder or institution.

Differences Between Checking and Savings Accounts

:max_bytes(150000):strip_icc():saturation(0.2):brightness(10):contrast(5)/a-man-using-credit-card--online-shopping---electronic-banking-1133639578-a2751011b96f4883bef7031c37a65bd5.jpg)

:max_bytes(150000):strip_icc()/PritchardJustinJacketSized-5b7485a846e0fb0050436534.jpg)

:max_bytes(150000):strip_icc()/CSP_ER9-ErikaR.-5942904ef41f4814a94dd1a5c1c03f32.jpg)

Checking and savings accounts are the bank accounts you use most often. They both hold money for safekeeping but have different features, and it’s essential to understand the differences between these accounts and when to use each one.

Checking vs. Saving

Used for payments

Best for money you plan to spend soon

Used to save for the future

Good for money you don’t need right away

Checking Accounts

A checking account is designed for frequent transactions, and you can use your money in a variety of ways.

- Automatic electronic payments: If you pay regular bills, you can have funds deducted from your checking account automatically each month, eliminating the need to manually pay bills. For example, you can set up automatic mobile phone bills, mortgage payments, and insurance premiums by providing your checking account details to anybody you want to pay.

- Debit card payments: A debit card allows you to spend from your checking account balance easily. You can swipe the card for in-person purchases or enter your card information for online payments.

- Online bill pay with your bank: In addition to having billers deduct money from checking, you can send payments from your checking account on demand. Log in to your account and set up a payment, and your bank will mail a check or send the funds electronically.

- ATM withdrawals: Your debit card also works at ATMs for cash withdrawals (and even deposits in some cases).

- Paper checks: Although they’re not as popular as they used to be, checks can still be an inexpensive and easy payment option.

Checking Account Interest

Traditional checking accounts don’t pay interest on your account balance. However, some checking accounts pay interest, and those accounts may be appealing if you keep a significant amount of money in checking. To find interest-bearing checking, look for:

- Online banks that pay interest on checking balances: For example, Alliant Credit Union’s High-Rate Checking account pays a modest amount of interest.

- Local banks and credit unions with “rewards” checking accounts: Be aware that you may need to meet strict criteria to earn a meaningful amount. For example, you may need to use your debit card 12 times per month or satisfy other requirements.

For most people, checking accounts aren’t a significant source of interest earnings. If you keep a relatively small amount in checking (or if interest rates are low), you may be better off focusing on free checking accounts that don’t drain your account balance. Calculate how much you’ll actually earn before you get too excited about interest checking.

Checking Account Fees

Checking accounts are notorious for charging fees. But you can dodge those fees with free checking accounts. There are two ways to bank without paying monthly charges:

- Find a truly free checking account: To do so, check with local banks and credit unions, which may not have monthly maintenance charges. Some online banks also provide free checking.

- Qualify for fee waivers: At most banks, you can avoid fees by meeting certain criteria. For example, if you set up direct deposit into your account (from employer), you may be able to bank fee-free.

Checking accounts charge a variety of fees:

- Monthly maintenance charges: Flat-dollar fees that come out of your balance every month. It’s hard to imagine a situation where it makes sense to pay those fees.

- Overdraft charges: Transaction fees for spending more than you have in your account. The bank might “lend” you money or allow payments to go through even when your account is empty. You need to repay those amounts, and you’ll typically pay additional overdraft charges.

- Insufficient funds fees: Similar to overdraft charges, but those might hit your account even when the bank doesn’t cover payments for you. If you try to spend more than you have, an insufficient funds fee may apply.

- Additional fees: You may have to pay ATM charges for using certain ATMs, although some banks rebate those fees. What’s more, some banks charge for requests like wire transfers, replacement debit cards, and stop-payment requests.

Savings Accounts

Savings accounts are designed to keep your money safe while paying a modest amount of interest on your account balance:

- Grow your money: Savings accounts typically pay interest, so you earn money on the cash you’re not using. Compare that to checking accounts, which usually do not pay interest.

- Separate long-term money: If you’re saving for a rainy day or other financial goals (like a vacation or down payment), savings accounts can help. By removing funds from your checking account, you’re less likely to overspend. It can even make sense to use multiple savings accounts for various goals.

Access Your Savings

When you need to spend your savings, you can access funds in several ways. However, federal law limits how often you can make certain withdrawals from savings. You can make up to six withdrawals per month, but certain types of transactions are unlimited.

- Transfer to checking: You can move money from your savings account to a checking account when you plan to spend. That’s almost instant if both accounts are at the same bank, and it typically takes a few days to move money from one bank to another.

- Cash withdrawals: If you use cash and your bank provides an ATM card, you can get cash out of your savings account at an ATM. Likewise, you can visit a bank branch and request cash. You can withdraw funds with an ATM or bank teller as often as you want.

- Request a check: Banks can also print checks payable to you. You can then deposit those checks at a different bank or credit union. There is no limit to the number of checks you receive when the checks are payable to you.

Savings Account Fees

Savings accounts tend to be less expensive than checking accounts, but it’s critical to review fee schedules before you open an account. Monthly fees are not very common, but ATM fees are still a reality. Plus, if you make more than six withdrawals (again, ATM withdrawals don’t count toward that limit), you may face excess transaction fees.

Beyond Checking and Savings Accounts

Checking and saving accounts aren’t the only accounts available at banks. Get familiar with other options.

Money market accounts Money market accounts have features of both checking and savings accounts. They often pay more than checking accounts, and they allow limited spending. Depending on your bank, a money market account might provide a checkbook, a debit card, or online bill payment options.

Certificates of deposit (CDs) are for money that you don’t intend to spend for at least six months. CDs typically pay more than savings accounts, but you need to commit to leaving your funds untouched for six months, one year, or more. If you cash out early, you may need to pay a penalty.